- Ackman-Ziff Market Update

- Posts

- Ackman-Ziff Opportunity Zone Equity Structuring Overview

Ackman-Ziff Opportunity Zone Equity Structuring Overview

Jordan Brustein & Andew Rudy

September 11, 2025

AZ OZ Equity Structuring Overview

With the inclusion of “Opportunity Zone 2.0” as part of the Trump administration’s Big Beautiful Bill, we wanted to provide the latest capital markets underwriting standards and cost of capital for institutional Opportunity Zone (“OZ”) equity allocation.

Before diving in, a quick disclaimer: the analysis below is presented on a pre-tax basis and incorporates certain assumptions about the program’s benefits. Ackman-Ziff is not a tax consultant, and we encourage you to speak with Novogradac or your own advisors to fully understand the tax implications.

The Big Picture

Sourcing development equity has become harder today than at any time since the 2008-2010 cycle. Opportunity Zones are no exception, despite being designed to encourage investment into pioneering zip codes.

The way institutional OZ equity is structured and priced looks very different from traditional opportunistic equity funds. Why? Because IRR isn’t the sole driving metric. OZ investments are “build-to-core,” and that changes everything:

Longer Investment Duration: Investors must plan for a 10-year hold, making it extremely difficult to underwrite high-teens IRRs.

Capital Preservation Over Appreciation: OZ capital is derived from capital gains that would have been taxed otherwise, so allocators lean more toward stability than potential large upside.

Focused on AM Fees: Equity allocators don’t see OZ funds as a path to tremendously large promotes, especially given the 10-year hold mandate, they’re motivated by long-term asset management fees.

The result: while there’s interest in OZ investments, and the appetite for common equity in OZ development deals remains slightly greater than merchant-build equity strategies, OZ capital in the form of common equity is still hard to come by. More often, we see OZ equity structured as preferred equity or pre-TCO and post-TCO recapitalizations.

Today’s Merchant Build Math

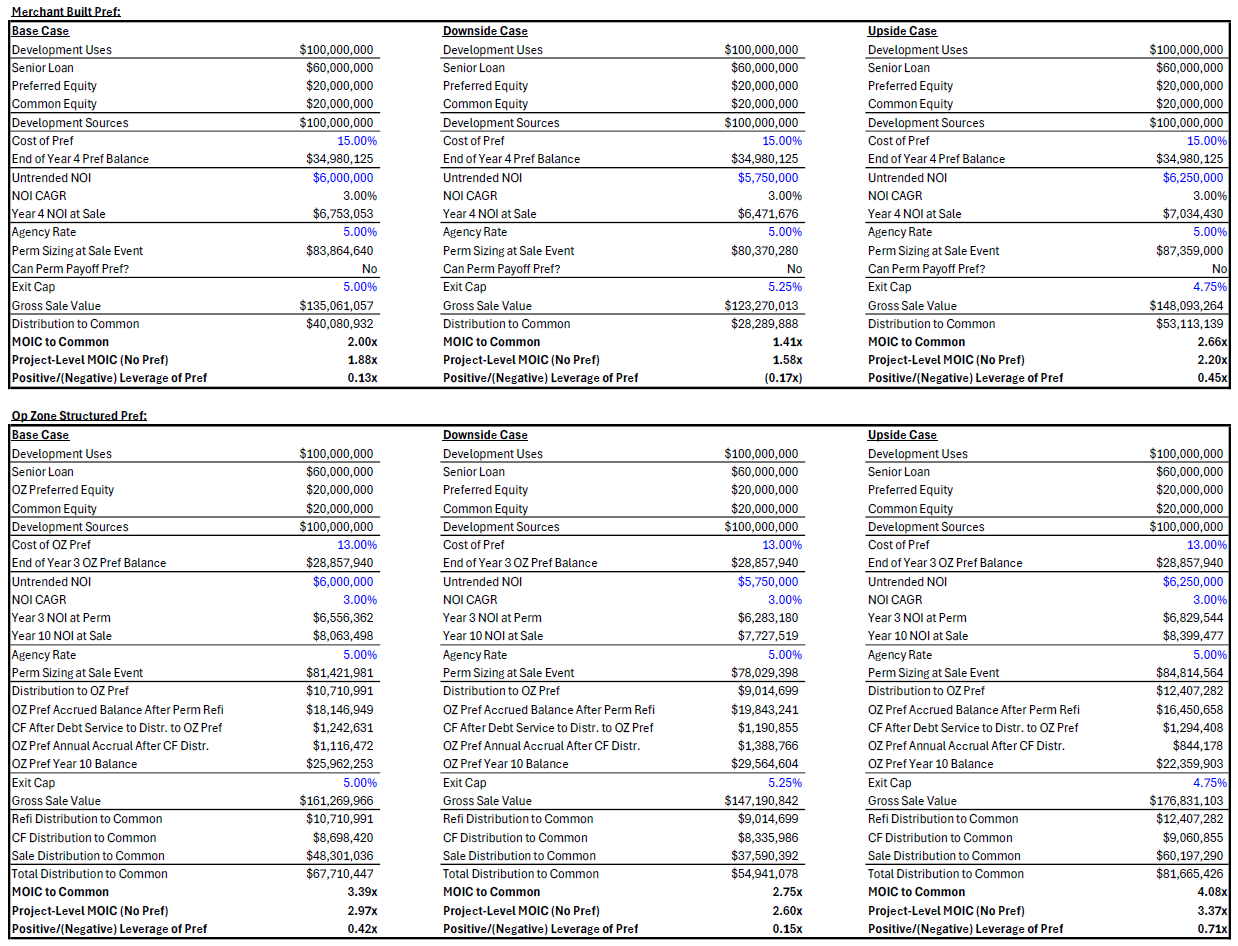

Take a $100M development that stabilizes at an untrended NOI of $6.0M, resulting in a 6.0% untrended return-on-cost (“ROC”). With stabilized cap rates at 5.0%, that’s only a 100 bps spread, well shy of the 125-175 bps premium most equity investors require.

The typical capital stack today looks like:

$60M construction loan [60% LTC | 10% debt yield]

$20M preferred equity [80% LTC | 15% fully accruing rate of return]

$20M of developer/common equity

At stabilization/sale in Year 4, the preferred equity accrues to $35M, resulting in $95M of total leverage. From the pref equity partner’s perspective, that equates to a 6.30% untrended ROC to their last dollar of leverage, a much more palatable 130 bps spread to the stabilized cap rate value.

Developers are understandably struggling with this level of leverage. (a) They must contribute $20M of common equity (substantially higher than the traditional 90-10 or 95-5 JV equity structure) and (b) in order to pencil, underwriting must assume NOI growth of 3% CAGR, reaching $6.75M at exit. At a 5.0% exit cap, this translates to a $135M valuation.

Upon sale, after repaying the construction loan, the preferred equity partner receives a $35M distribution (1.5x MOIC), while the developer receives $40M (2.0x MOIC). If the preferred equity were instead structured as common equity, the levered MOIC would be 1.86x. That incremental 0.14x of positive leverage created by layering in preferred equity offers little benefit to the developer/common equity.

This dynamic has effectively stalled the vast majority of ground-up development deals.

How OZ Preferred Equity Works (And Why It Works)

Now let’s re-run the numbers using an OZ preferred equity structure:

$100M total capitalization

$6.0M untrended NOI

$60M construction loan [60% LTC | 10% debt yield]

$20M OZ Preferred Equity [80% LTC | 7.5% yield without accrual | 50% of total equity required]

$20M Developer Common Equity [6.0% ROC | 50% of total equity required]

Ackman-Ziff has been structuring OZ Preferred Equity as pari passu and pro rata on cash flow distributions from refinance and operations, with the priority IRR return to the OZ Preferred Equity partner solved at the sale event in Year 10. Ackman-Ziff has successfully negotiated a catch-up to the common equity to the same IRR as the OZ Preferred Equity return, followed by a 20% profit share to the OZ Preferred Equity above the catch-up. The OZ Preferred Equity typically prices at a ~13% IRR which is 200-300 bps cheaper than traditional merchant-build pref, while still retaining certain common equity like features.

Assume permanent financing is 5YR T + 125bps spread (5.00% fixed), 30-year amortization, and 1.25x DSCR resulting in an approximately 8.0% debt yield sizing of ~$85M of permanent financing on the trended NOI in Year 3. OZ Preferred Equity receives 50% of the cashout proceeds – a $12.5M distribution at refinance, reducing its accrued capital account by $12.5M.

Going forward, the OZ Preferred Equity Partner receives 50% of all cash flow from operations which contributes and reduces the nominal dollars to their 13% total accrued priority IRR at exit in Year 10. Without trending NOI for distributions made from operations, the OZ Preferred Equity partner’s outstanding capital balance to solve for a 13% IRR in Year 10 is equal to approximately $27.5M.

Assuming NOI grows to $8M and the property sells at a 5.0% cap value of $160M in Year 10:

OZ Preferred Equity is distributed (i) $12.5M distribution from refinance, (ii) $1.25M annual distribution from operations, and (iii) $27.5M Distribution from Sale for a total return of $48.75M (2.44x MOIC)

The Common Equity is distributed (i) $12.5M distribution from refinance, (ii) $1.25M annual distribution from operations, and (iii) $47.5M Distribution from Sale for a total return of $68.75M (3.44x MOIC)

Importantly, both sides earn the same IRR prior to exit, only prioritizing distributions from sale to the OZ Preferred Equity partner to their low-teens returns, then the Common Equity is distributed the lion’s share of remaining available cash flow.

Why This Works

This structure functions much like an insurance product. It allows sponsors to increase leverage without being forced to sell or refinance at stabilization. If things go well with permanent financing, the pref gets paid down early. If not, there’s additional runway for rents to grow or rates to reset.

Compared to traditional merchant development:

OZ Pref Equity delivers stronger positive leverage while providing greater downside protection to the sponsor than merchant-built strategies (see examples scenarios).

The 10-year hold creates additional structuring flexibility. We’ve received term sheets that include separate waterfalls for refinance and sale, or even provisions to convert OZ Pref into common equity at a crystallization event.

Final Thoughts

We believe structured OZ Preferred Equity is accretive in today’s market. With construction loans sizing to 10% debt yields and permanent financing to 8% debt yields, there is now a stronger case for meaningful cash-out at the permanent financing than in prior cycles.

At Ackman-Ziff, we’ve developed proprietary models to stress-test these structures, and the results consistently show that, even in downside scenarios, common equity benefits from positive leverage over the life of the deal. We’d be glad to be a resource as you think through these strategies.

Sensitized High-Level Development Returns

X

|

Client With Large 1031 Exchange Requirement

Also, please note that we are working with a client who has a $150-$200M 1031 exchange requirement. They are seeking core/core-plus industrial and retail opportunities in the major Midwest markets and Dallas, TX. Please let us know if you have any opportunities you would like us to share with them.

Jordan Brustein; Andrew Rudy

M: (JB) 516-996-7722; (AR) 858-947-8738